Introduction

Choosing the right type of health insurance is just as important as choosing the right coverage amount.

Many buyers are confused between two popular options:

- Family Floater Health Insurance

- Individual Health Insurance

Both provide medical coverage, but they work differently and are suitable for different situations.

So which one should you choose in 2026?

In this guide, we’ll compare Family Floater and Individual Health Insurance plans, explain their advantages and disadvantages, and help you determine which option best fits your family’s healthcare needs and budget.

Affiliate Disclosure:

Some links may be affiliate links. We may earn a commission at no extra cost to you.

Table of Contents

- What Is Individual Health Insurance?

- What Is Family Floater Health Insurance?

- Key Differences

- Pros and Cons

- Which Option Is Better for You?

- Real-Life Examples

- Common Mistakes to Avoid

- FAQ

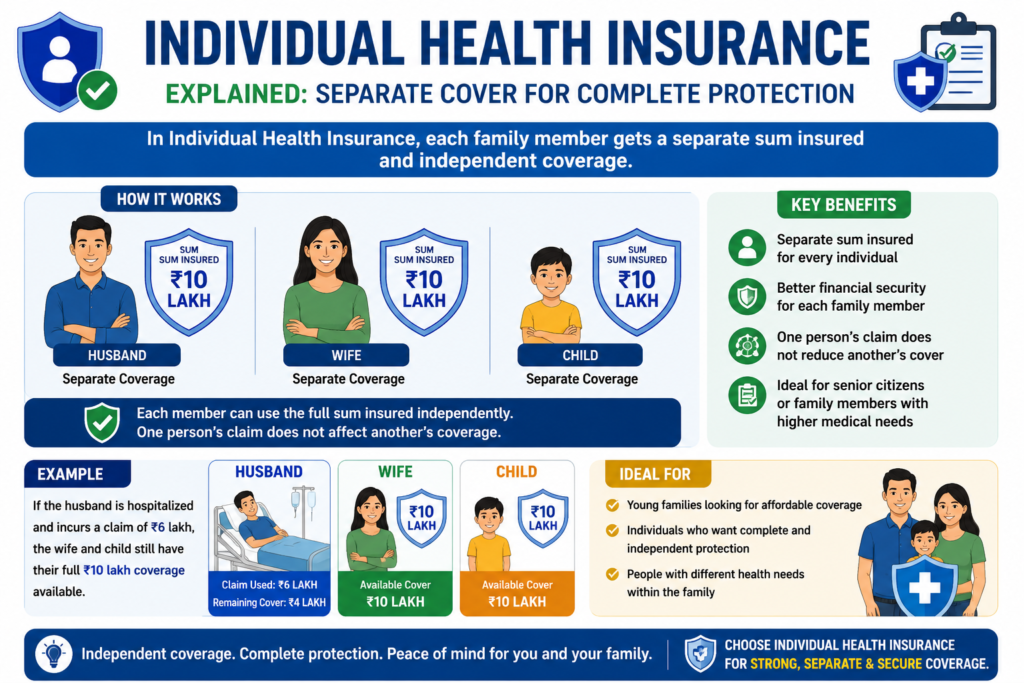

What Is Individual Health Insurance?

Individual Health Insurance provides a separate sum insured for each insured person.

Example:

- Husband: ₹10 lakh cover

- Wife: ₹10 lakh cover

Each individual receives independent coverage.

Advantages

✔ Separate coverage

✔ No sharing of sum insured

✔ Better for older individuals

✔ Lower risk of exhausting coverage

Disadvantages

✖ Higher premiums

✖ Multiple policies to manage

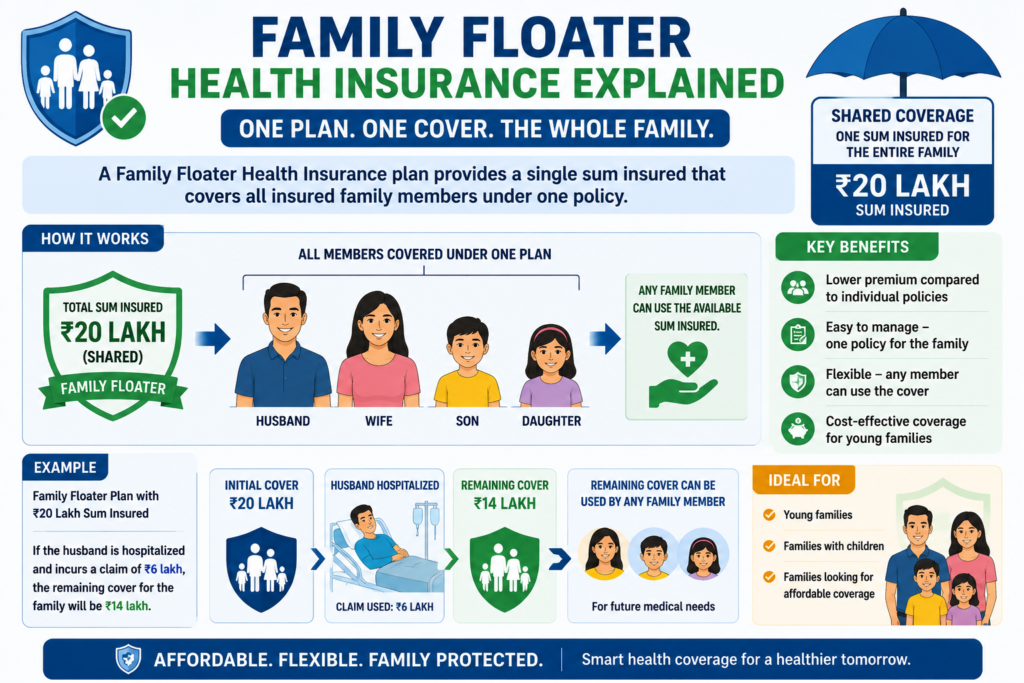

What Is Family Floater Health Insurance?

A Family Floater policy provides one shared sum insured for all covered family members.

Example:

Family Floater:

₹20 lakh cover

Covered Members:

- Husband

- Wife

- Child

Any family member can use the available sum insured.

Advantages

✔ Lower premium

✔ Easier policy management

✔ Suitable for young families

✔ Higher overall affordability

Disadvantages

✖ Coverage is shared

✖ Large claims may reduce available cover

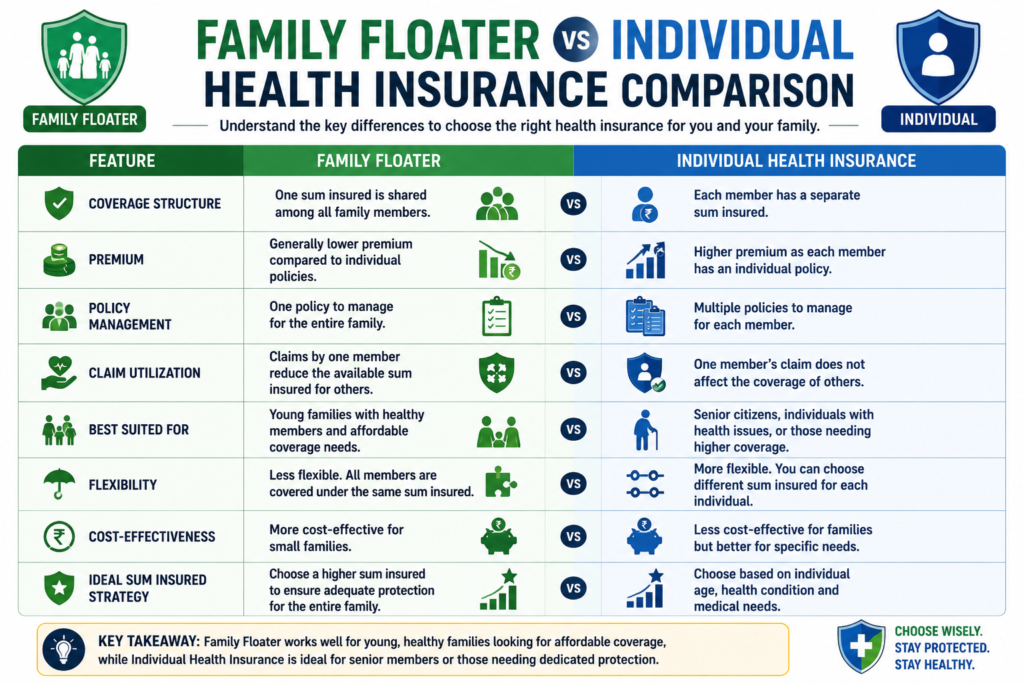

Family Floater vs Individual Health Insurance Comparison

| Feature | Family Floater | Individual |

|---|---|---|

| Coverage | Shared | Separate |

| Premium | Lower | Higher |

| Policy Management | Easier | Multiple Policies |

| Best for Young Families | Yes | Sometimes |

| Best for Senior Citizens | No | Yes |

| Coverage Availability | Shared Pool | Dedicated Cover |

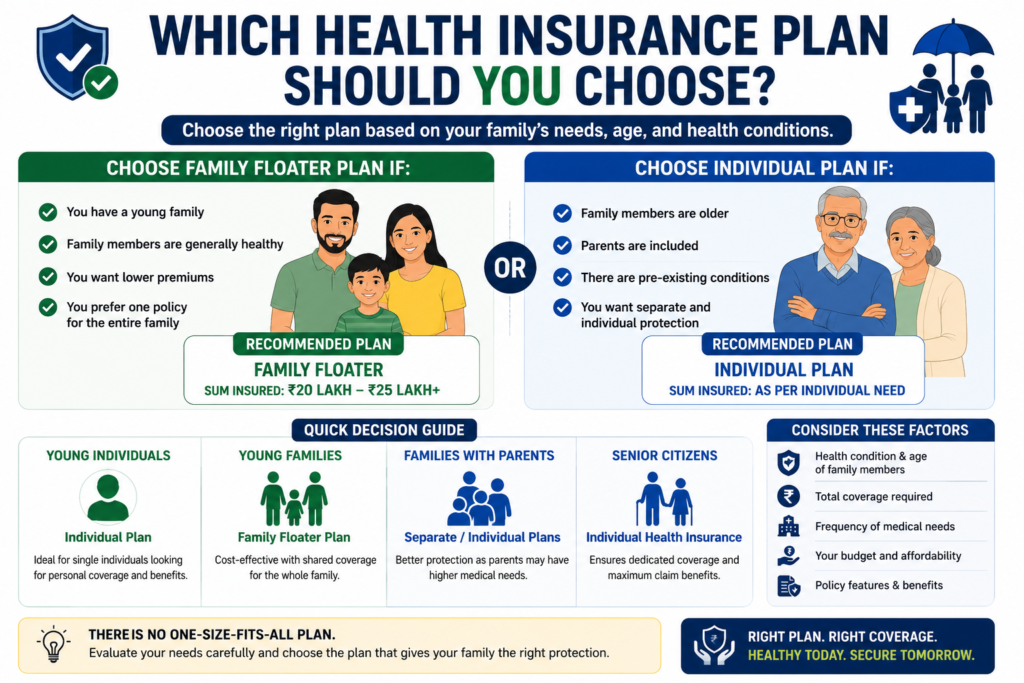

Which Option Is Better for You?

Choose Family Floater If:

- You have a young family

- Family members are generally healthy

- You want lower premiums

- You want one policy for everyone

Example

Rahul (32), Priya (30), and their child.

Recommended:

Family Floater ₹20–25 lakh

Choose Individual Health Insurance If:

- Family members are older

- Parents are included

- There are pre-existing conditions

- You want separate protection

Example

Amit (58) and Sunita (55)

Recommended:

Separate individual policies

Real-Life Examples

Example 1: Young Couple

Age:

30 & 28

Recommended:

Family Floater

Reason:

Lower premium and shared risk.

Example 2: Family with Children

Age:

35, 33, and two children

Recommended:

Family Floater ₹25 lakh+

Reason:

Cost-effective coverage.

Example 3: Senior Citizens

Age:

65 and 62

Recommended:

Individual Plans

Reason:

Higher claim probability.

Compare Health Insurance Plans

Before purchasing a policy, compare:

- Premiums

- Waiting periods

- Network hospitals

- Claim support

- Coverage benefits

👉 Compare plans through Policybazaar.

(Link)

Common Mistakes to Avoid

Including Elderly Parents in a Young Family Floater

This may increase premiums significantly.

Choosing Coverage Based Only on Premium

Lower premiums may mean insufficient protection.

Ignoring Medical History

Always consider existing health conditions.

Not Reviewing Policy Features

Compare benefits carefully.

Our Recommendation

Young Individuals

Individual Policy

Young Families

Family Floater

Families with Parents

Separate Policies

Senior Citizens

Individual Health Insurance

For most families in India, a Family Floater policy works well during younger years, while separate coverage becomes more important as age and healthcare needs increase.

External References

For insurance regulations and consumer awareness information, refer to the Insurance Regulatory and Development Authority of India (IRDAI).

Our Experience

At Nivesh Saathi, we regularly evaluate health insurance products, policy structures, claim trends, and healthcare costs to help readers make informed insurance decisions.

Conclusion

Both Family Floater and Individual Health Insurance plans have advantages.

The right choice depends on:

- Age

- Family size

- Medical history

- Budget

- Coverage needs

Choose the option that provides adequate protection without compromising your family’s financial security.

Compare Plans Now

Compare premiums, features, and coverage options through Policybazaar.

(Link)

Related Articles

FAQ

Which is better, family floater or individual health insurance?

It depends on age, family size, and medical history. Family Floaters are generally suitable for young families, while Individual plans are often better for senior citizens.

Is family floater cheaper than individual health insurance?

Yes, in many cases Family Floater plans have lower premiums than purchasing separate individual policies.

Can parents be included in a family floater plan?

Yes, but doing so may significantly increase premiums, especially if parents are older.

Is ₹20 lakh family floater enough?

For many young families, ₹20–25 lakh can provide reasonable protection, depending on city and healthcare costs.

Can I switch from family floater to individual health insurance later?

Many insurers allow policy changes during renewal, subject to terms and conditions.

What is the biggest disadvantage of a family floater plan?

The sum insured is shared among all covered members.

Is individual health insurance better for senior citizens?

Often yes, because coverage is dedicated to each person and claim probability is higher.

How do I choose the right health insurance plan?

Compare coverage, waiting periods, network hospitals, claim support, exclusions, and premiums before purchasing.

About the Author

Shashikant Pawar is the founder of Nivesh Saathi and writes practical guides on insurance, loans, investments, and personal finance for Indian readers.

About Nivesh Saathi

Nivesh Saathi helps Indians make smarter financial decisions through trustworthy, easy-to-understand financial education and product comparisons.

Disclaimer

This article is for educational purposes only and should not be considered insurance advice. Please review policy documents carefully and consult a qualified advisor before purchasing insurance.