Introduction

Medical emergencies can put significant financial pressure on families. A single hospitalization can cost lakhs of rupees, making health insurance an essential part of financial planning.

Choosing the best health insurance plan for your family is not just about finding the lowest premium. You need adequate coverage, access to quality hospitals, claim support, and protection against rising healthcare costs.

In this guide, you’ll learn how family health insurance works, the features to compare, recommended coverage amounts, common mistakes to avoid, and how to choose the right plan for your family in 2026.

Affiliate Disclosure:

Some links may be affiliate links. We may earn a commission at no extra cost to you.

Table of Contents

- Why Families Need Health Insurance

- Types of Family Health Insurance Plans

- Features to Compare

- Recommended Coverage by Family Size

- How to Choose the Best Family Plan

- Real-Life Examples

- Common Mistakes to Avoid

- FAQ

Why Families Need Health Insurance

Healthcare costs continue to rise every year.

A family health insurance plan helps:

✔ Cover hospitalization expenses

✔ Protect savings

✔ Access cashless treatment

✔ Reduce financial stress

✔ Provide long-term healthcare security

Example

A family of four facing a ₹10 lakh hospitalization bill can avoid a significant financial burden with adequate health insurance coverage.

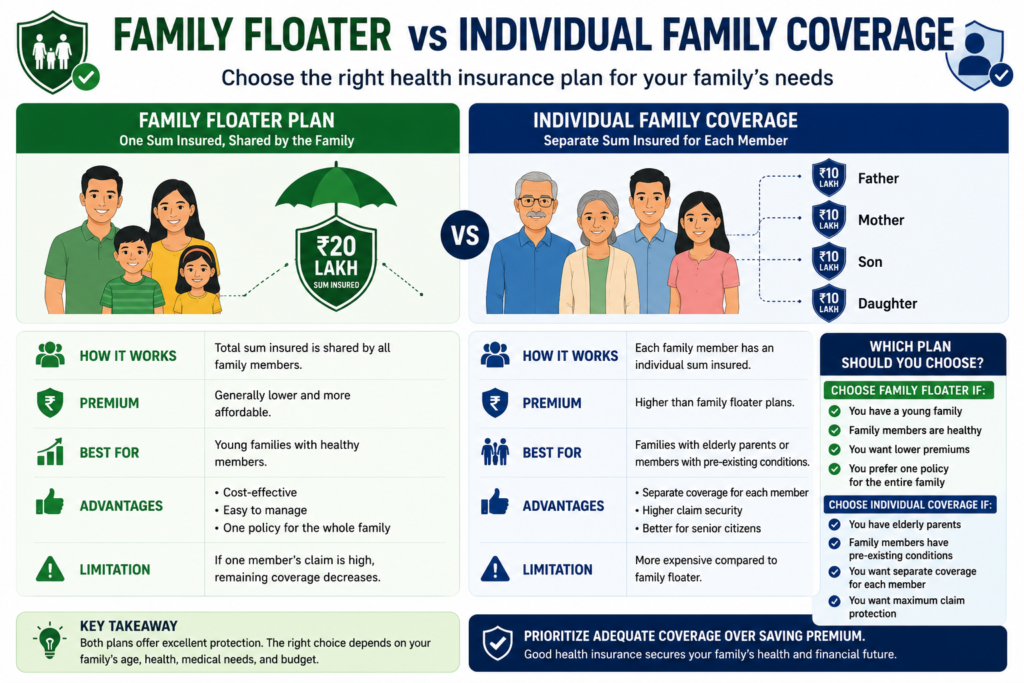

Types of Family Health Insurance Plans

Family Floater Plan

One shared sum insured for all family members.

Best For:

- Young families

- Couples with children

Advantages

✔ Lower premium

✔ Easy policy management

Individual Family Coverage

Separate policies for each member.

Best For:

- Families with elderly parents

- Members with pre-existing conditions

Advantages

✔ Dedicated coverage

✔ Better for high-risk individuals

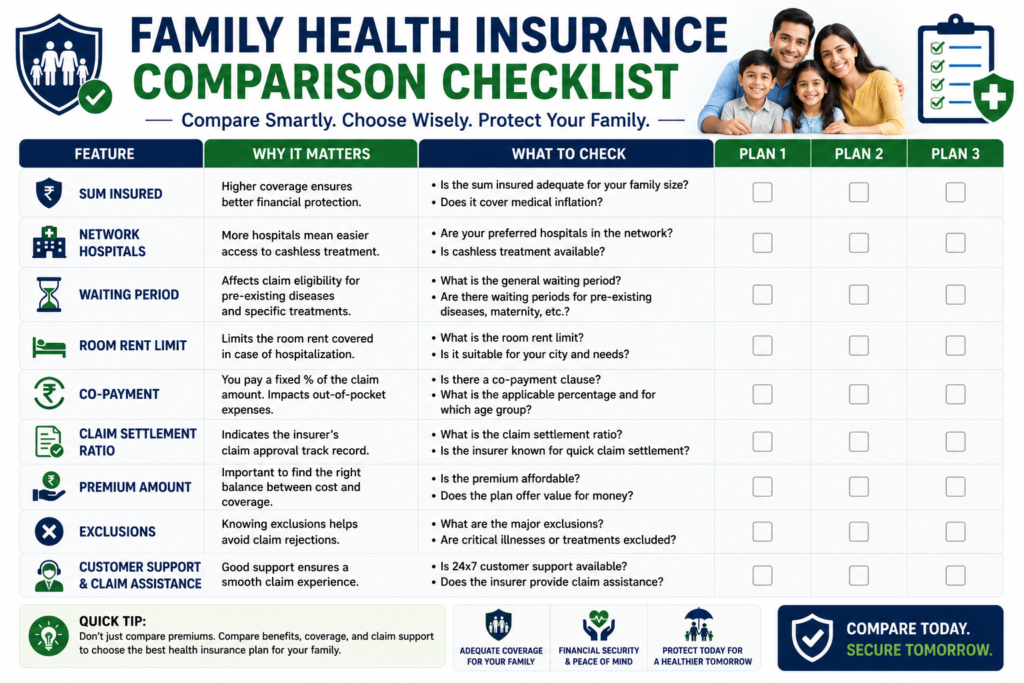

Key Features to Compare

Before selecting a family health insurance plan, compare:

| Feature | Why It Matters |

|---|---|

| Sum Insured | Determines coverage amount |

| Network Hospitals | Supports cashless treatment |

| Waiting Period | Impacts claim eligibility |

| Room Rent Limit | Affects claim payout |

| Co-Payment | Impacts out-of-pocket expenses |

| Claim Support | Improves claim experience |

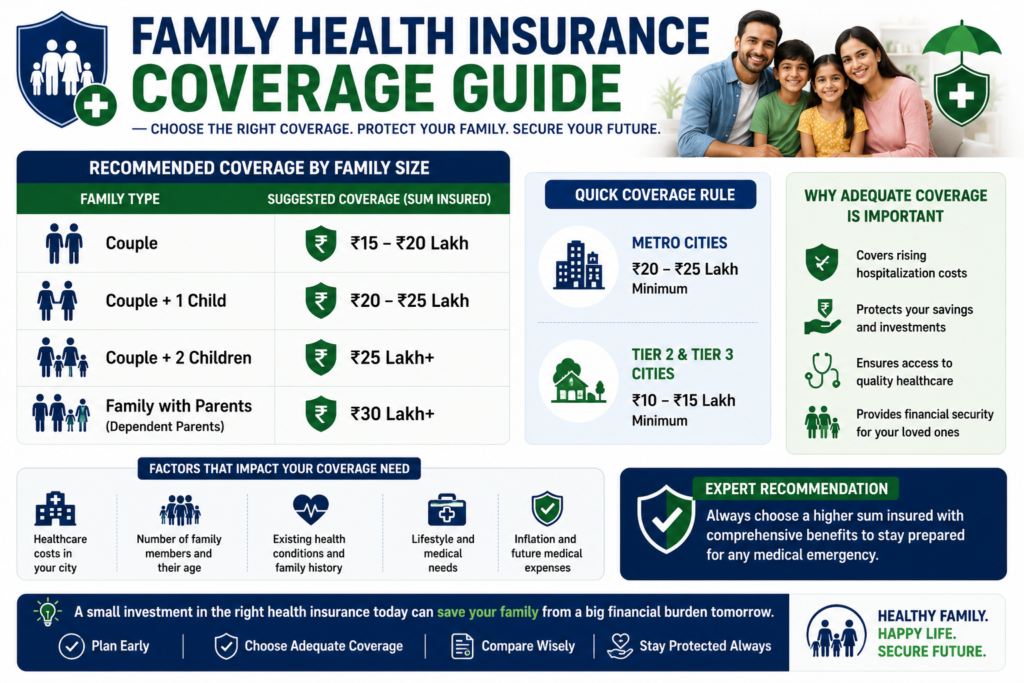

Recommended Coverage by Family Size

| Family Type | Suggested Coverage |

| Couple | ₹15–20 lakh |

| Couple + 1 Child | ₹20–25 lakh |

| Couple + 2 Children | ₹25 lakh+ |

| Family with Parents | ₹30 lakh+ |

Quick Coverage Rule

Metro Cities:

₹20–25 lakh minimum

Tier 2 & Tier 3 Cities:

₹10–15 lakh minimum

How to Choose the Best Family Health Insurance Plan

Step 1

Assess family healthcare needs.

Step 2

Estimate required coverage.

Step 3

Compare plan benefits.

Step 4

Check hospital network.

Step 5

Review claim support.

Step 6

Compare premiums and value.

Real-Life Examples

Example 1

Rahul and Priya

Age:

32 and 30

Child:

1

Recommended:

Family Floater ₹20 lakh

Reason:

Young healthy family.

Example 2

Amit and Sunita

Age:

58 and 55

Recommended:

Separate Individual Plans

Reason:

Higher claim probability.

Example 3

Family with Two Children

Recommended:

Family Floater ₹25 lakh+

Reason:

Cost-effective and adequate coverage.

Compare Family Health Insurance Plans

Before buying a plan:

✔ Compare coverage

✔ Compare premiums

✔ Compare benefits

✔ Compare claim support

👉 Compare family health insurance plans through Policybazaar.

(Link)

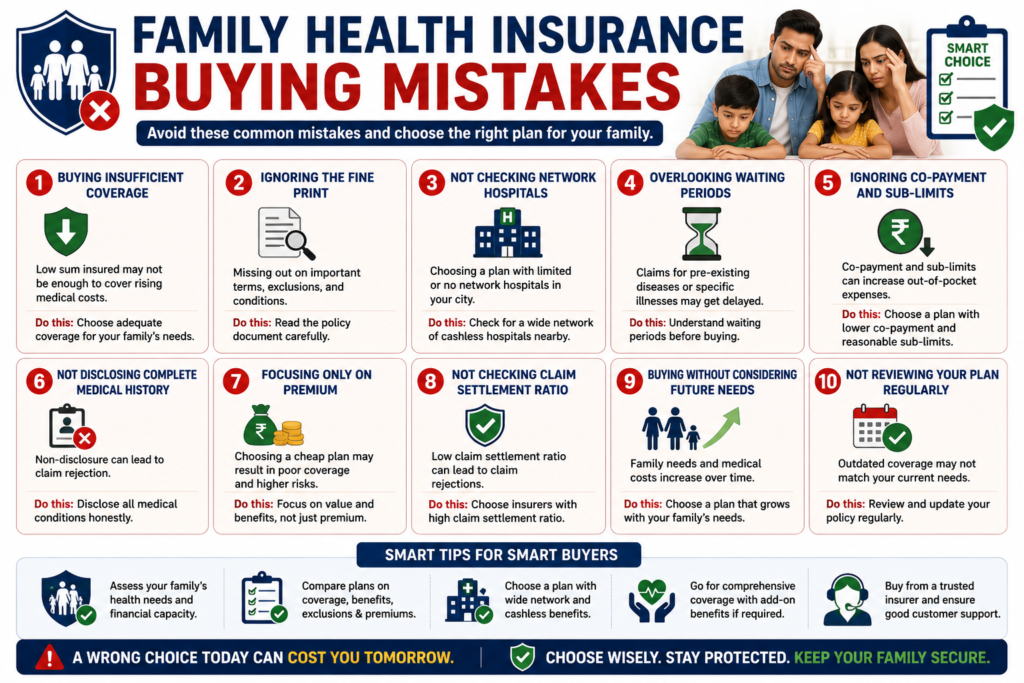

Common Mistakes to Avoid

Choosing the Cheapest Plan

Coverage matters more than premium alone.

Ignoring Medical Inflation

Healthcare costs continue to rise.

Choosing Low Coverage

Underinsurance can create financial stress.

Ignoring Waiting Periods

Review policy terms carefully.

Not Checking Network Hospitals

Cashless access is important.

Safe Health Insurance Buying Tips

✔ Buy early

✔ Choose adequate coverage

✔ Review exclusions

✔ Compare multiple plans

✔ Consider super top-up plans

Our Recommendation

Young Families

Family Floater ₹20–25 lakh

Families with Parents

Separate Coverage

Metro City Families

₹25 lakh+ Coverage

High-Income Families

₹50 lakh+ Protection Including Top-Up Plans

External Reference

For insurance regulations and consumer awareness information, refer to IRDAI.

Our Experience

At Nivesh Saathi, we regularly evaluate health insurance plans, healthcare costs, policy features, and claim support factors to help readers choose suitable family health insurance coverage.

Conclusion

The best family health insurance plan is one that balances affordability, adequate coverage, hospital access, and long-term financial protection.

Choose a plan that protects your family’s health without compromising your financial goals.

Compare Plans Now

Compare premiums, features, and coverage options through Policybazaar.

(Link)

Related Articles

- How Much Health Insurance Cover Do You Need in India? (2026 Guide)

- Family Floater vs Individual Health Insurance: Which Is Better in 2026?

FAQ

Which health insurance is best for families in India?

The best plan depends on family size, age, healthcare needs, and coverage requirements.

Is family floater health insurance better?

For many young families, Family Floater plans provide cost-effective protection.

How much health insurance cover should a family of four have?

Many experts recommend ₹20–25 lakh or higher depending on city and healthcare costs.

Can parents be included in family health insurance?

Yes, but separate coverage may be more suitable for older parents.

What is the ideal family health insurance coverage?

For many urban families, ₹20–25 lakh is considered a reasonable starting point.

Is employer health insurance enough?

Employer coverage may not always provide sufficient protection.

Should I buy a super top-up plan?

A super top-up plan can increase coverage at a relatively lower premium.

How do I compare family health insurance plans?

Compare coverage, waiting periods, network hospitals, claim support, exclusions, and premiums.

About the Author

Shashikant Pawar is the founder of Nivesh Saathi and writes practical guides on insurance, loans, investments, and personal finance for Indian readers.

About Nivesh Saathi

Nivesh Saathi helps Indians make smarter financial decisions through trustworthy, easy-to-understand financial education and product comparisons.

Disclaimer

This article is for educational purposes only and should not be considered insurance advice. Please review policy documents carefully before purchasing insurance.