Introduction

As parents age, healthcare needs increase and medical expenses can become a significant financial burden.

Many families realize the importance of health insurance for parents only after facing a major hospitalization or medical emergency.

The right health insurance plan can help protect your parents from rising healthcare costs while safeguarding your family’s finances.

In this guide, you’ll learn how to choose health insurance for parents, recommended coverage amounts, important features to compare, common mistakes to avoid, and practical tips for finding the right policy in 2026.

Affiliate Disclosure:

Some links may be affiliate links. We may earn a commission at no extra cost to you.

Table of Contents

- Why Parents Need Health Insurance

- Challenges of Buying Health Insurance for Parents

- Key Features to Compare

- Recommended Coverage by Age Group

- Family Floater vs Separate Policy for Parents

- Real-Life Examples

- Common Mistakes to Avoid

- FAQ

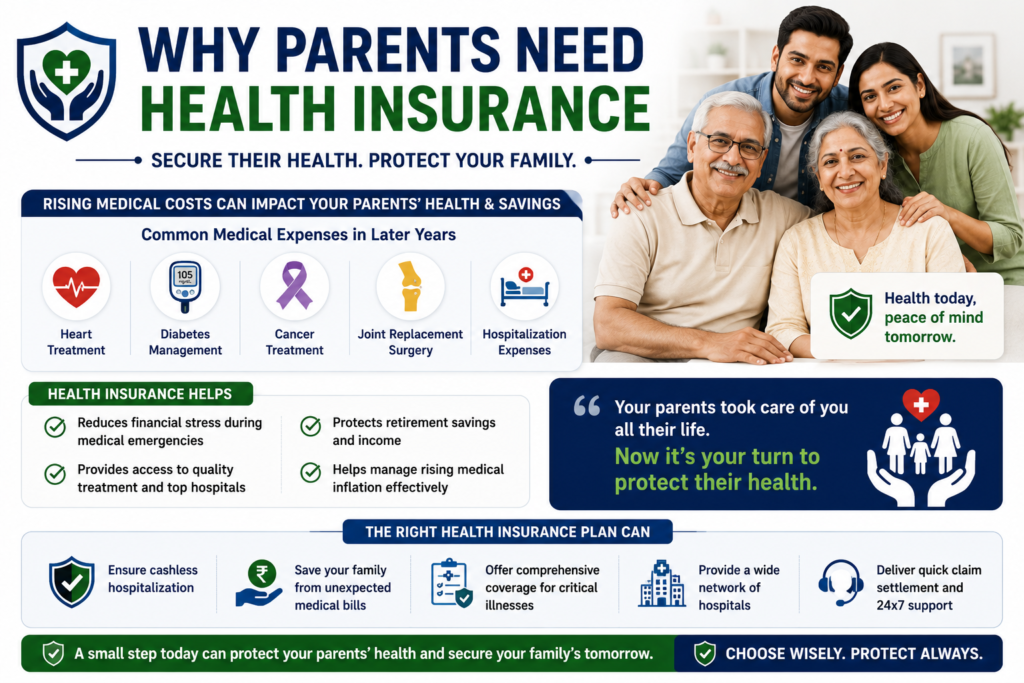

Why Parents Need Health Insurance

Healthcare costs tend to increase with age.

Common medical expenses include:

- Heart treatment

- Diabetes management

- Cancer treatment

- Joint replacement surgery

- Hospitalization expenses

Health insurance helps:

✔ Reduce financial stress

✔ Access quality hospitals

✔ Protect retirement savings

✔ Manage rising medical inflation

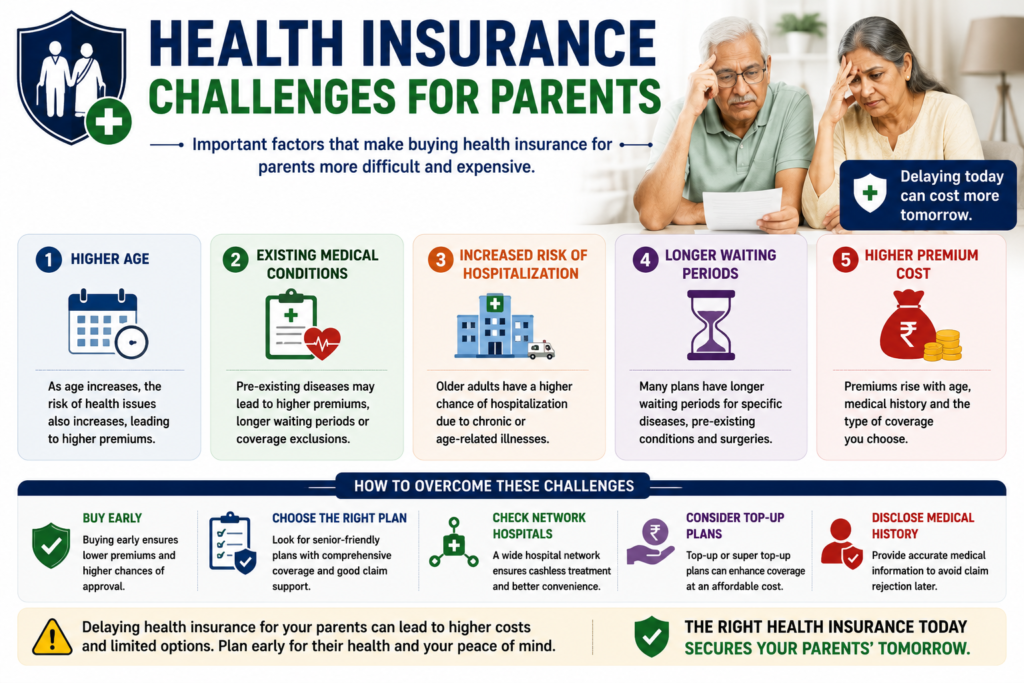

Challenges of Buying Health Insurance for Parents

Health insurance for parents can be more expensive because:

- Higher age

- Existing medical conditions

- Increased hospitalization risk

- Longer waiting periods

However, delaying purchase may increase costs further.

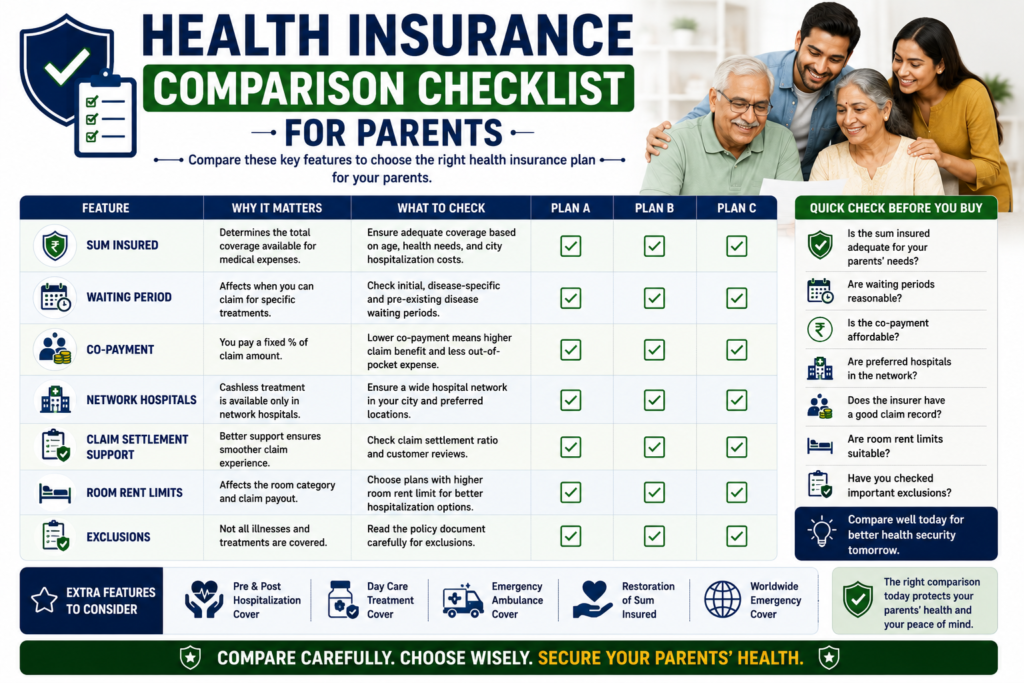

Key Features to Compare

Before choosing a policy, compare:

| Feature | Why It Matters |

|---|---|

| Sum Insured | Coverage amount available |

| Waiting Period | Impacts claim eligibility |

| Co-Payment | Affects out-of-pocket expenses |

| Network Hospitals | Supports cashless treatment |

| Claim Settlement Support | Better claim experience |

| Room Rent Limits | Influences claim payout |

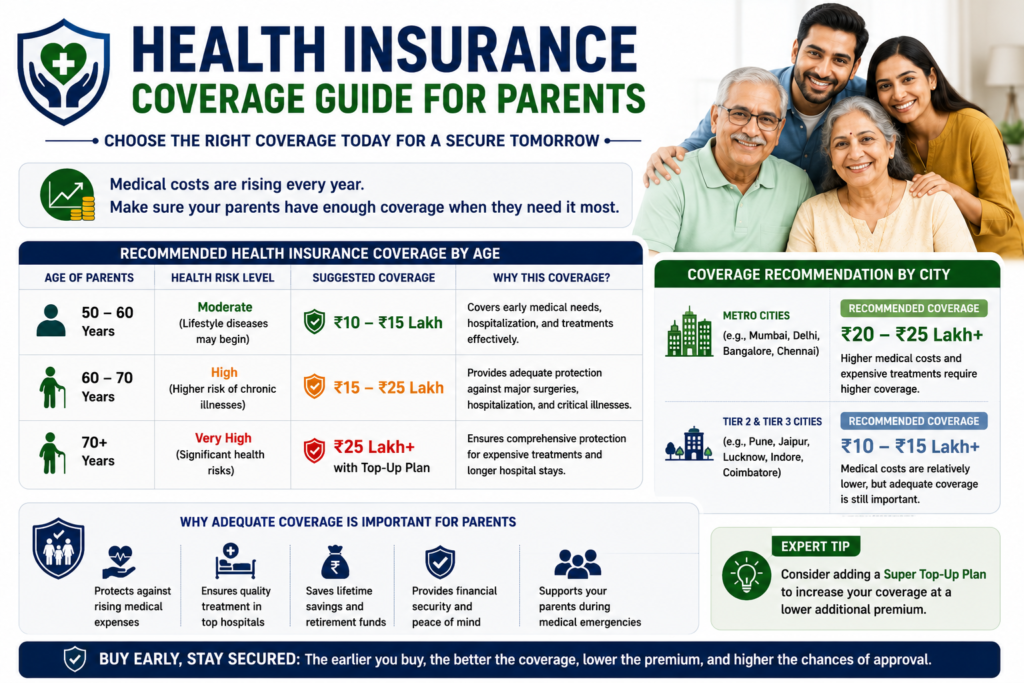

Recommended Coverage by Age Group

| Age | Suggested Coverage |

|---|---|

| 50–60 | ₹10–15 lakh |

| 60–70 | ₹15–25 lakh |

| 70+ | ₹25 lakh+ |

Metro Cities

Recommended:

₹20–25 lakh+

Tier 2 & Tier 3 Cities

Recommended:

₹10–15 lakh+

Family Floater vs Separate Policy for Parents

Family Floater

Advantages:

✔ Single policy

✔ Easier management

Disadvantages:

✖ Premium increases significantly when elderly parents are included.

Separate Policy

Advantages:

✔ Dedicated coverage

✔ Better claim protection

✔ More suitable for older parents

Our Recommendation

In most cases, elderly parents should have separate health insurance policies.

Real-Life Examples

Example 1

Parents:

Age 55 and 53

Recommended:

₹15 lakh coverage

Reason:

Moderate healthcare risk.

Example 2

Parents:

Age 67 and 64

Recommended:

₹25 lakh coverage with top-up plan.

Reason:

Higher medical expenses.

Example 3

Parents:

Age 72 and 70

Recommended:

Separate individual policies with comprehensive coverage.

Compare Health Insurance Plans

Before purchasing:

✔ Compare premiums

✔ Compare waiting periods

✔ Compare hospital networks

✔ Compare claim support

👉 Compare health insurance plans for parents through Policybazaar.

(Link)

Common Mistakes to Avoid

Buying Low Coverage

Medical costs can rise significantly with age.

Ignoring Waiting Periods

Review policy conditions carefully.

Choosing Only Based on Premium

Coverage quality matters.

Including Parents in Family Floater Without Evaluation

This may increase costs and reduce efficiency.

Delaying Purchase

Premiums generally increase with age.

Safe Health Insurance Buying Tips

✔ Buy early

✔ Choose adequate coverage

✔ Review exclusions

✔ Compare multiple plans

✔ Consider super top-up plans

✔ Disclose medical history honestly

Our Recommendation

Parents in Their 50s

₹10–15 lakh coverage

Parents in Their 60s

₹15–25 lakh coverage

Parents Above 70

₹25 lakh+ with top-up plans

Metro City Residents

Higher coverage recommended due to healthcare costs.

External Reference

For consumer awareness and insurance regulations, refer to IRDAI.

Our Experience

At Nivesh Saathi, we regularly analyze health insurance products, claim trends, healthcare costs, and policy features to help families choose suitable coverage for their parents.

Conclusion

Health insurance for parents is one of the most important financial protections a family can have.

Buying adequate coverage early can help manage healthcare costs, reduce financial stress, and provide peace of mind during medical emergencies.

Compare Plans Now

Compare premiums, features, and coverage options through Policybazaar.

(Link)

Related Articles

- How Much Health Insurance Cover Do You Need in India? (2026 Guide)

- Family Floater vs Individual Health Insurance

- Best Health Insurance Plans for Families in India

FAQ

Which health insurance is best for parents in India?

The best plan depends on age, health conditions, coverage needs, and budget.

How much health insurance coverage do parents need?

Many experts recommend ₹15–25 lakh or more depending on age and city.

Can parents be included in a family floater policy?

Yes, but separate coverage is often more suitable for older parents.

Is health insurance expensive for senior parents?

Premiums generally increase with age and medical risk.

What is a super top-up plan?

A super top-up plan provides additional coverage above a specified deductible.

Should parents buy separate health insurance?

In many cases, separate policies provide better protection and claim flexibility.

Can pre-existing diseases be covered?

Many plans provide coverage after completion of waiting periods.

When should parents buy health insurance?

The earlier, the better, as premiums and eligibility are usually more favorable at younger ages.

About the Author

Shashikant Pawar is the founder of Nivesh Saathi and writes practical guides on insurance, loans, investments, and personal finance for Indian readers.

About Nivesh Saathi

Nivesh Saathi helps Indians make smarter financial decisions through trustworthy, easy-to-understand financial education and product comparisons.

Disclaimer

This article is for educational purposes only and should not be considered insurance advice. Please review policy documents carefully before purchasing insurance.